Cake Box Holdings PLC ($CBOX.L)

£62MM compounder with solid financials, a quality brand and impressive capital allocation by owner-operator

Quick preface: This happens to be the third consecutive UK consumer discretionary stock that I cover because there is a lot of value to be captured due to UK’s current macro conditions. However, coming write-ups will cover different types of businesses such as $TCM.CO, a danish kitchen manufacturer at all-time lows and $WATR.L, a company providing pipe leak detection and plumbing services across the whole of US.

Business Overview

Premium, egg-free and fresh cream cakes by season, celebration and design

Cake Box was founded in 2008 by Sukh Chamdal and Pardip Dass as a provider of egg-free, delicious cream cakes that serve nearly all consumers, even people restricted by diets or religious beliefs, without compromising taste or texture. As of 2023 Cake Box has over 200 franchise stores across the UK, serving as their customers. What Cake Box does is that it manufactures the secret-recipe cakes in their three operational centres and sell them to franchisees, which in turn makes the franchise proposition very attractive. So Cake Box itself doesn’t operate any stores, which gives it great opportunities to offer full training and ongoing support to franchisees, expand store estate and franchise growth strategically, grow their product range and improve their data-driven approach as well as multi-channel expansion.

Segments and Products

Cake Box sells cakes through three kinds of outlets: franchises, shopping-centre kiosks and supermarket kiosks. Franchises are their main outlets and Cake Box shows it by setting up demanding and professional standards for every existing and potential franchisee. Their process of hiring franchisees to represent their brand is rigorous and when chosen, franchisees receive full training, access to Cake Box’s network of professionals, help with pre-opening marketing and access to Cake Box’s franchise forums every two months. As a franchisee, you operate a simple retail business model and importantly don’t have to worry about baking. The start-up cost for a high street franchise is also low, with average investment payback of 18-24 months. In FY23, 20 new franchise stores opened, the amount supermarket kiosks increased to 18 and the amount of franchisees grew to 44. Cake Box also saw a 4.1% increase in online sales through their new, UX focused website.

Cake Box offers a service called “Click and Collect”, which means you can order and personalise a cake online and have it ready to be picked up on very short notice. The personalisation, opted for by 90% of customers, done on-site, on-demand is also a differentiating factor, as other retailers require days to personalise a cake. Cake Box’s product range includes cake slices (serving 1-2), normal-sized cakes and cheesecakes (both serving 8), platter cakes (serving 64), loaf cakes and cupcakes.

Outlook

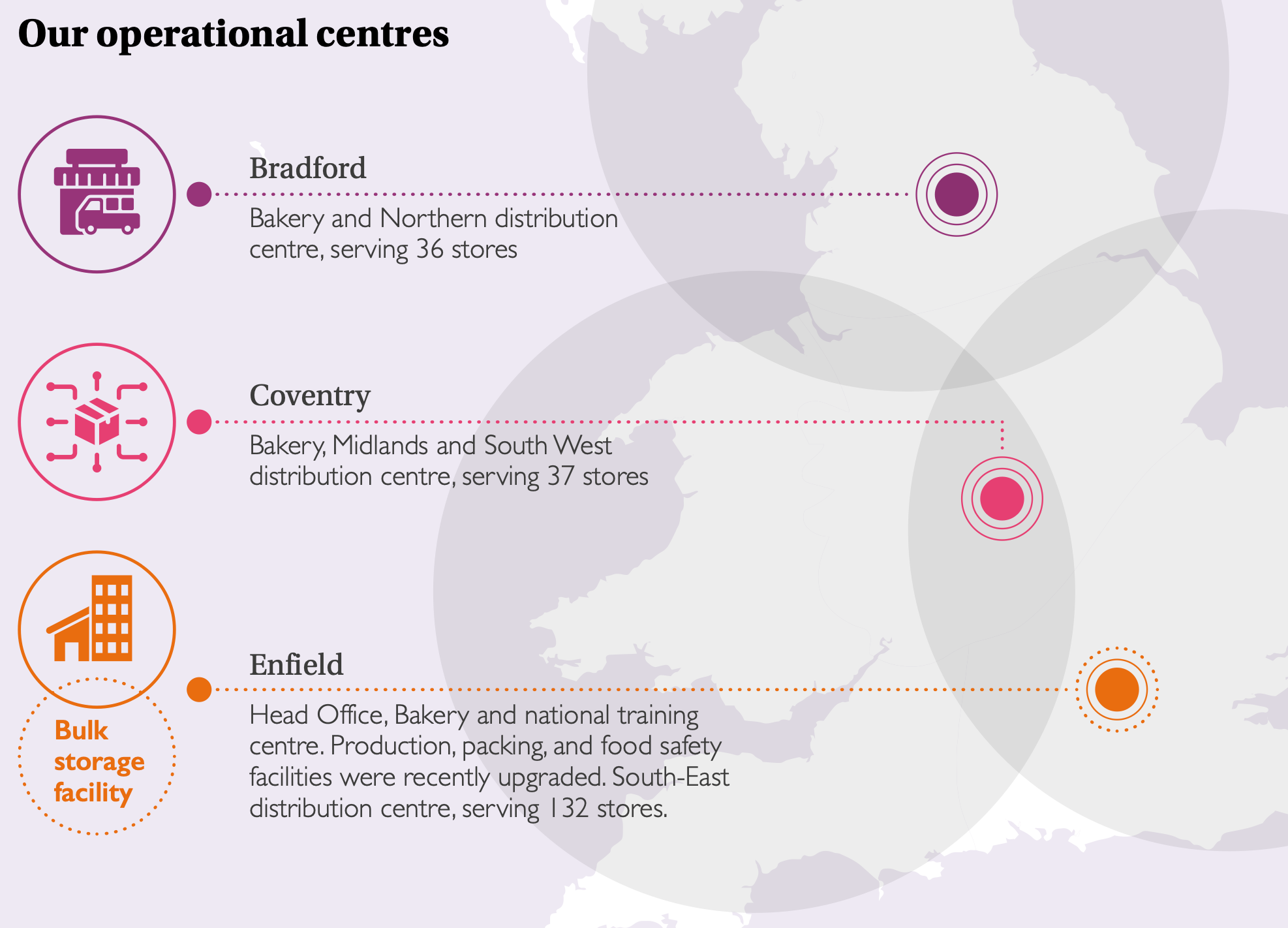

As pictured above, Cake Box is most prominent in the south of England around their Enfield head office, and have lots of underserved locations left around the rest of the country as well as in Wales and Scotland. Their goal is to add around 70 stores in two to three years, mainly in mainland Britain, and their long-term vision is having 400 stores across the UK. Even at 400 stores I don’t think any kind of saturation will be experienced and the pipeline for growing to that number within the UK is very clear.

If they can get a strong foothold in all the underserved areas in the UK as well as ramp up their pop-up style kiosk rollout in a sophisticated and strategic way, therefore maximising growth opportunities, I believe they are well positioned for continued growth. Birthdays and other celebrations are a great source of recurring revenue and I don’t see how cake sales would ever rapidly decrease. Even a recession would probably serve Cake Box well as less people celebrate at restaurants and hotels and instead celebrate at home. I’ve also done some empirical research and concluded that everyone who has tried Cake Box’s cakes has loved them, would buy them again and would recommend them, which regarding consumer discretionary is a great sign of a loved and in-demand product.

At the start of FY23 a profit margin warning was released which said inflation was eating into their profits. However, in the latest 10-K management sees that the unprecedented level of inflation is starting to soften up, in turn supporting margin progression in the mid-term. Cake Box is also positioned as a premium retailer, so the lowest price isn’t necessary to their offering, and in a 2022 earnings call CEO Chamdal saw price hikes as a realistic measure to protect both Cake Box’s and the franchises margins in the short-term. That turned into reality when Cake Box were able to pass on some price rises to franchisees who in turn were able to raise sales prices to customers albeit at a lower rate than the food retail sector without having a significant impact on volumes.

One concern with the company is the “scandal” surrounding Co-founder and previous CFO Dass and their previous auditor. After an impressive 4x in under 2 years since Covid started, the “accounting issues” led to the stock price plunging over 60% in under two months. The accounting issues consisted of false entries in the cash flow statement, delayed reporting of a website breach, bookkeeping curiosities and the auditor resigning after becoming “concerned about the robustness of the Company’s control and governance frameworks“. None of this however proved to have been done purposely, Cake Box has now appointed a seasoned and professional new CFO and since the scandal they have been stressing non-stop about strengthening their internal audit function. So this storm is behind us and won’t bother the company’s future but is still imprinted in the stock price, which makes for a possible opportunity.

Financials

Cake Box is trading at 8x EV/EBITDA and 12x EV/FCF which are at a good sale versus 5-year averages but still not dirt-cheap. However, these multiples reflect the 22% 5-year CAGR in revenue growth, increasing gross margins (50%), 17% 5-year average net margins (excluding FY23), net-debt-to-FCF of 0.3 and great returns on invested capital. The stock did a ridiculous 230% CAGR (only 1.5 years but used for reference) from the start of covid to the scandal bust, and no real harm was made to the business. It was slightly overvalued post-covid but in turn it might be slightly undervalued now.

Cake Box boasts a strong balance sheet with £7.4M in cash balance and the group’s only debt is £1.3M in mortgages secured by its freehold properties. The franchise model has a relatively low cost base so the board is very comfortable with current liquidity levels and cash balance despite the unprecedented events of the last three years. There are 40M shares outstanding and no dilution has happened since the IPO in 2018. For FY23 the company paid a 5.5p-per-share dividend and probably will continue to give out a portion of earnings to shareholders in the future.

Management

CEO and Co-founder Sukh Chamdal, previously a consultant for a food equipment company focusing on high-volume food production, owns approximately 25% of shares and is therefore well aligned with shareholders. CFO Michael Botha was appointed in 2023 after a small-scale “scandal” after which former CFO and Co-founder Dass had to resign. Botha seems very rational and experienced, as he has 20 years of experience in senior finance and commercial roles for franchise businesses, most recently for one of the largest Domino’s franchise groups in the UK and Ireland. Chairman MBE Neil Sachdev, who joined in 2018, has extensive retail experience and serves as chair on a number of public sector bodies. Most executive and non-executive directors have been buying stock for the last year, bringing insider ownership up to almost 40% and boosting management’s incentives. What is fascinating is before the appointment of CFO Botha, all executive directors had at some point run their own franchise store, so they know exactly what franchisees and customers want and think.

Management’s capital allocation has historically been solid, with a 33.9% 10-year average ROIC, and created value in sophisticated ways for shareholders. Lately they have been paying a 5% dividend yield with a payout ratio of around 70% and opening lots of new outlets. However, I don’t mind if they scrap the dividend to reinvest into other initiatives driving long-term growth.

Valuation

Assumptions:

250 stores by FY26

2.5% like-for-like growth

9% average revenue growth up until FY28

Pretax margins returning to 2016-2022 average by FY25

25% tax rate and 15% discount rate

15x exit multiple

No share dilution

These assumptions, all fair leaning towards bull case, make up a 36% margin of safety and a 21% annualised return. The stock traded at 400p at its peak before the accounting issues versus 150p now, which signals that the company could be undervalued presently. The biggest catalyst is margin recovery and to which levels they recover in the coming years. Markets could react negatively to sustained levels of low net margins and that could present a great buying opportunity. For now, I’m monitoring Cake Box closely, as it stands on a solid financial base, has a growing business, a quality brand and experienced and incentivised management.

Thanks for reading, any feedback and all comments are very welcome as I still am quite new to the investing scene!

NOTE: This does not in any way constitute investment advice and is for educational purposes only. This is not a BUY or SELL recommendation, this is my own opinion. Any investment decisions should not be based on Smart Micro Caps articles. I encourage all readers to do their own due diligence and contact authorised professionals for advice.

Interesting idea, but how do you invest as a non UK investor? They seem to block you from going to their investor relations page if you are not a UK resident.